Credit Score: 3-digit number that decides your plans

29 Apr 2024 5 mins Personal Finance

The credit score is a three-digit number that can wield significant influence over our lives. If we miss out on payment installments, credit score damage is one of the significant factors banks warn us about. From securing loans for major purchases to determining the interest rates we pay, understanding credit scores is essential for anyone seeking financial stability. But what is a credit score and how does it affect our financial planning? And where does CIBIL come into the picture?

Let's try to break it down below:

What is CIBIL, and how is it associated with credit scores?

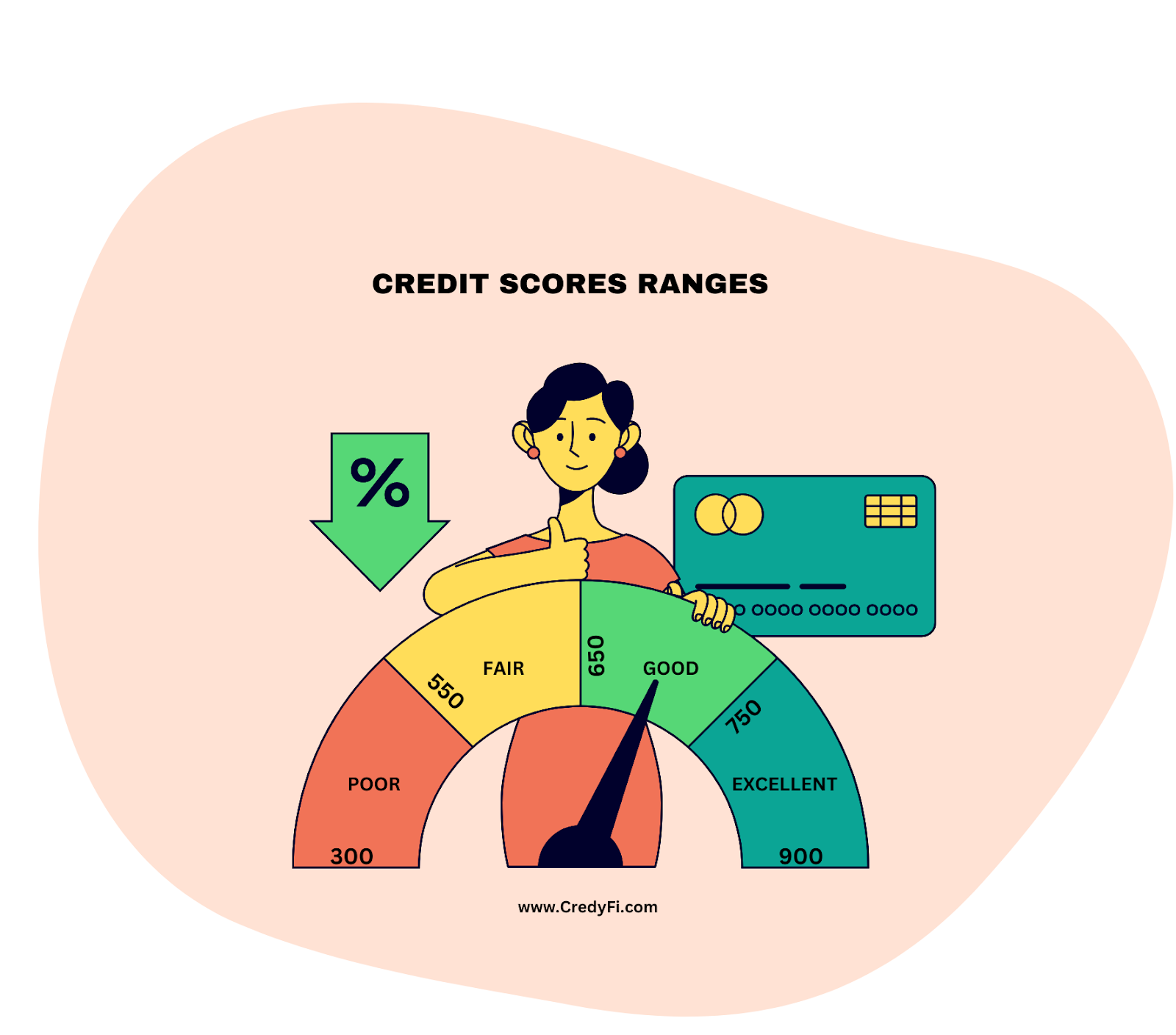

The credit score is a scale that checks the likelihood of the person paying back the loan amount taken. It is a 3-digit scale starting from 300 and ending at 900. It is created based on your credit history.

Credit Information Bureau (India) Limited (CIBIL) is a credit information company part of TransUnion. It is the first in India, authorized by the Reserve Bank of India (RBI), and covered under the 2005 Credit Information Companies Regulation Act. The credit score is calculated by CIBIL based on the credit information report.

What is the significance of credit score?

A credit score gives an idea of the creditworthiness of the borrower. The scores are based on past credit borrows and repayments. So, a lower score means the bank carries a risk of lending money to you, which could reduce your chances of getting the loan. A credit score of 750 and above can get approved loans 90% of the time. While a score of less than 650 is considered high risk for the lender.

A good credit score can give you the following advantages:

- All loans, from electronic items to home loans, are approved based on the credit score. A strong credit score means your loan applications are accepted more easily.

- You can negotiate the interest rate for your loans with a good score. You can get better rates with banks competing for you as a loanee.

- You become eligible for pre-approved loans and premium credit cards with high credit limits.

- Your chances for higher credit card and loan limits also improve with good scores.

- The possibility of longer tenure will be available for your loan approvals as you are more trustworthy based on your score.

How does CIBIL facilitate this?

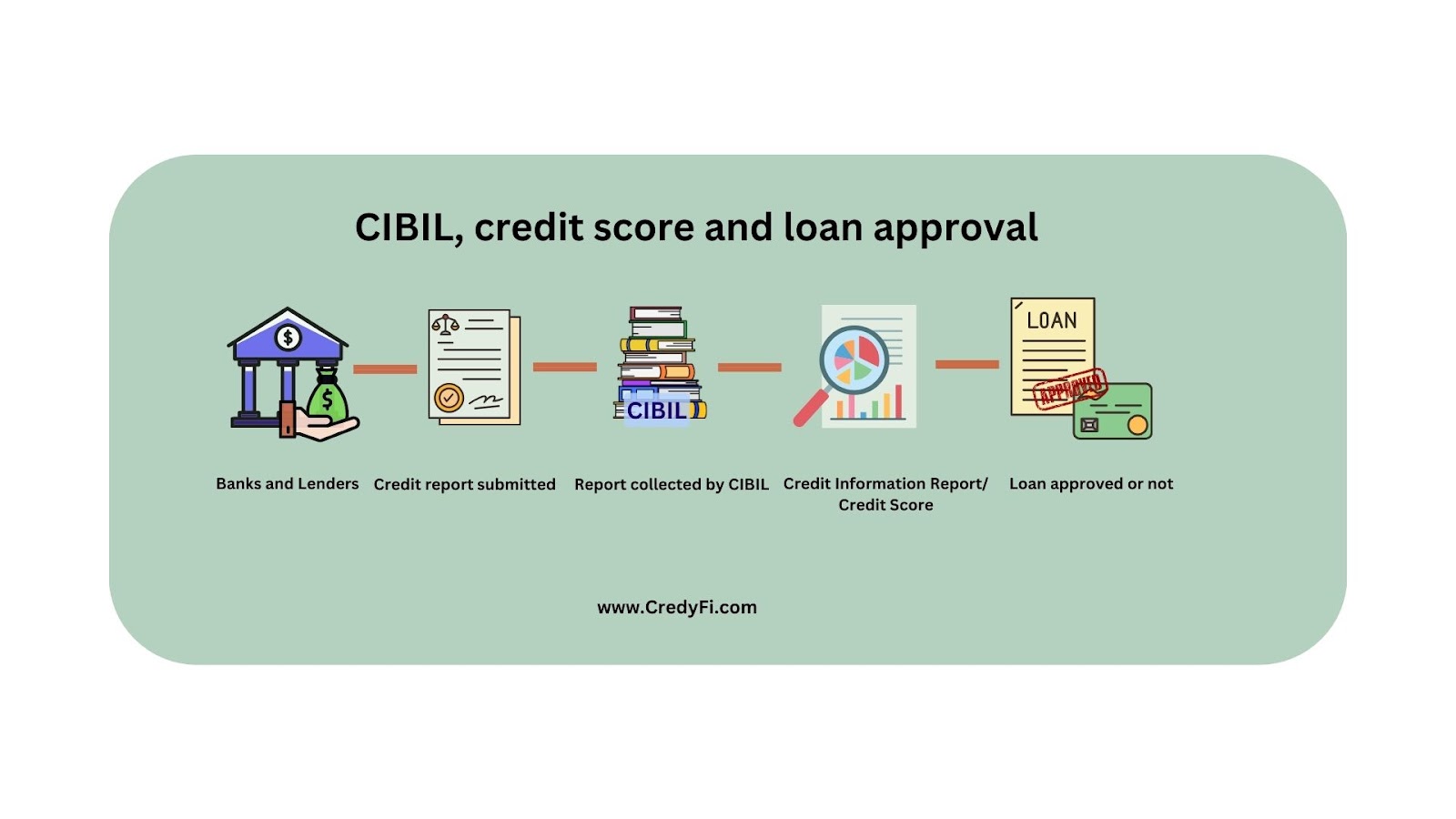

We saw how credit scores can affect our lives and will now see how CIBIL facilitates these scores. CIBIL is the company that collects and maintains credit information reports (CIRs) from banks and other financial institutions. The CIR contains the loan and credit card payment history of the individuals. Based on the history, the report provides the probability of the borrower defaulting on the payment. The CIR is used to generate the credit score.

So your borrowings, repayments, new loan requests, credit cards, and dues are all collected from various institutions and CIBIL compiles them to make the score. This report is available to download to check where your score is affected and can even raise disputes if you see any errors. This helps to stay on top of your current and future borrowing. CIBIL score can now be checked for free through almost all banking applications and other sites.

Can a person have a 0 CIBIL score?

CIBIL score scale starts from 300. So it's impossible for a person with a credit history to have a zero score. So if you have taken a loan or credit card from any point, it comes in your credit history and you will be assigned a score.

However, if you haven't taken any loans till now, your credit history is null and you won't have a CIBIL score. This makes it difficult for your future loan approvals and procedures. Since the lender or the creditor cannot understand your repayments, it's difficult for them to measure your creditworthiness. What you can do in that kind of instance is:

- Start small credits through secured and low-limit credit cards. Using the credit methods responsibly through regular repayment can help you build a good credit score. Secured credit cards are backed by fixed deposits and hence are quickly approved.

- For minor requirements like electronics purchases, take out easily manageable loans. Since the loan amount would be less, the tenure also would be around 12 months. This helps you relieve yourself of the loan quickly.

- If you have your parents or any family member already with the loan and a good credit score, join them to build your report. Becoming a co-applicant for a loan with these trustful borrowers helps you boost your score and build on good ground.

CIBIL credit score is the scale lenders and creditors use to check your trustworthiness in repaying the borrowed amount. The score is calculated by CIBIL, which manages the credit information from banks and financial institutions to create Credit Information Reports.

So, do not consider credit as always being heavy on the shoulders. Managing credits and debts to build your portfolio dramatically impacts your future financial planning. Through some thought and rearrangement, you can ensure your score never drops below the optimum range even if you missed a payment! Be aware and happy planning!!