Check these factors and secure your credit score

30 Apr 2024 6 mins Personal Finance

You are checking your CIBIL score and sure you haven’t missed a single payment any time. You are confident in having an excellent score and will have some negotiation for a better credit card. You check and see that your score is below 750! You pull out your credit report and realise that your existing credit utilisation is high and affecting you. What other factors can affect your score? What is a good score to have? Let's find the answers below:

What is the CIBIL score?

CIBIL, or credit score is a 3-digit scale showcasing your creditworthiness (likelihood of repayment). It is calculated based on the reports shared by the banks and financial institutions to CIBIL, where the scores are updated based on a couple of factors.

The score is considered by lenders and banks when you request loans and credit cards. A good credit score gives you added advantages such as negotiating the interest rate and getting premium credit cards.

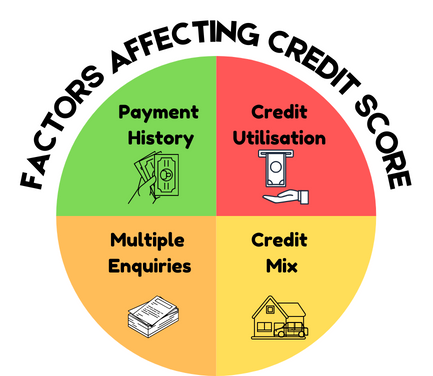

What are the factors affecting the CIBIL score?

A credit score is derived from the details of your account and enquiries in the CIBIL report based on the past 36 months of credit history.

There are four major factors affecting your credit score:

1.Payment History: Regular and frequent repayments are crucial.

Repaying your existing credit makes considerable differences in your credit report and the score. Late payments or not paying EMI will harm your future loans. If your payments are regular in total amount, it can significantly improve your score.

2.Credit Utilisation: Keep enough of a gap in your available credit.

Credit utilisation is the ratio of how much amount is borrowed from the total amount available to borrow. A lower utilisation ratio can help improve credit scores. The ideal credit utilisation ratio is less than 30%. That is, if you take the ratio of the amount you have borrowed and the available amount you can borrow, it should be less than 30%. For example, if you are sanctioned Rs. 1 Lakh to use as credit through card or loan, the healthy amount to use is Rs.30,000 (30% of 30,000). Using too much of your available sanctioned amount can give off the impression that you are at high risk of defaulting. This reduces your chance of securing another loan.

3.Credit Mix: Have diversity in your debts and credits.

The credit mix is the types of loans you have. A balanced mix of unsecured (loans without any collateral) like personal loans, credit cards, etc., and secured loans (loans against collateral) like home loans, auto loans, etc. affects your credit score positively. This diversity in the loan shows your ability to maintain both types of debts and gives an impression that you are creditworthy. Having a long credit history can also showcase that you are capable of managing your debts and that you can be trusted with the amount.

4.Multiple Enquiries: Avoid taking multiple loans in a short time.

Putting in hard inquiries can affect your CIBIL score. When you apply for a loan, the lender checks the CIBIL score. Having multiple loans in recent times can create an impression that your debt burden is increasing. This may be offputting for the lender as there is a difference in the expected behaviour and a sudden increase in debt.

These factors make your score go up and down, and lenders consider the credit score to check your reliability. With a higher credit score, you can enjoy benefits like comparing and negotiating your interest rates, getting higher limits and longer tenure for loans, premium credit cards, and more.

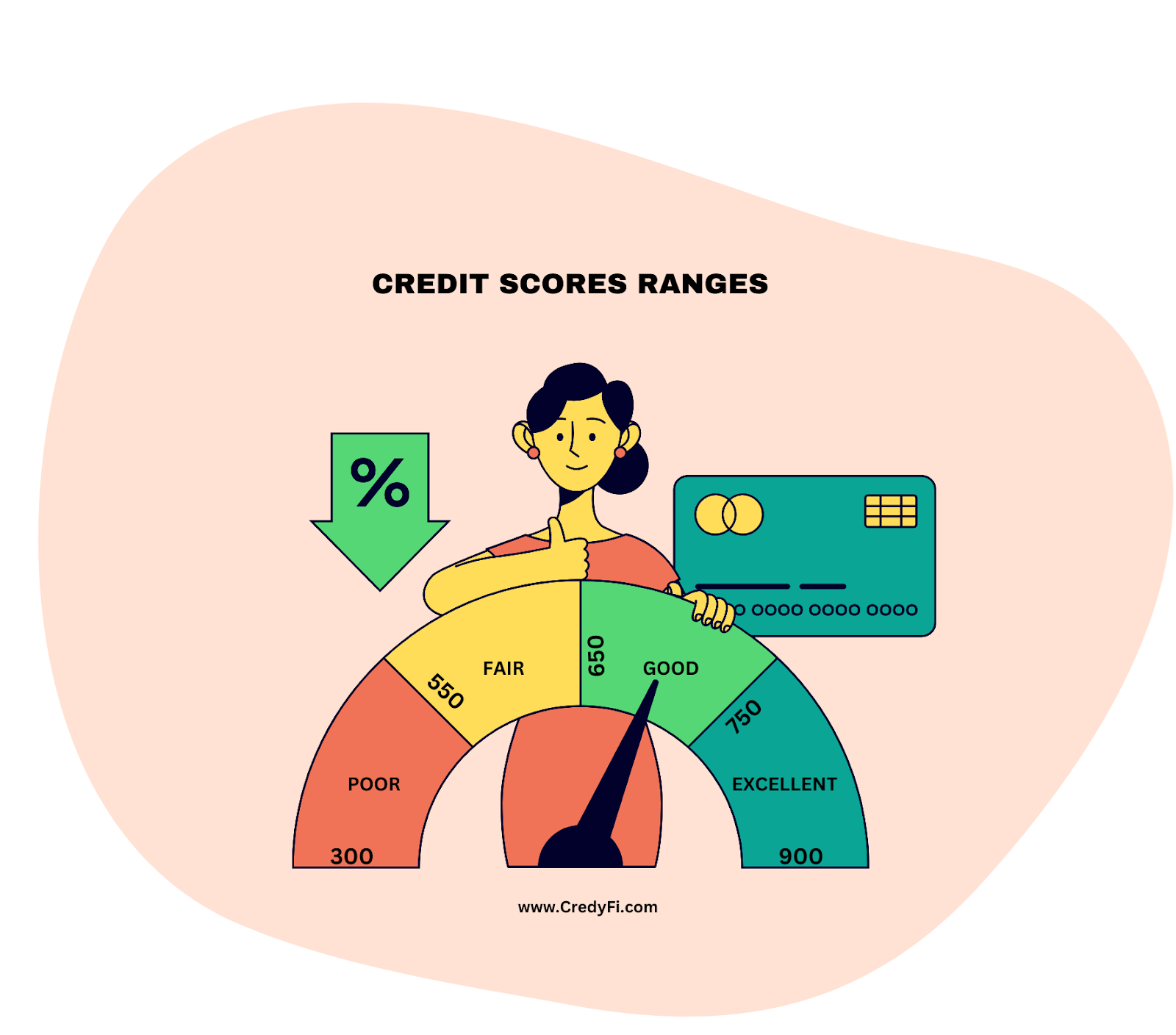

What are the ranges of credit scores?

- 750-900: This is the best range you can be. This range means you have excellent experience managing your credit and repayments. The credits you have taken are diverse, and you are always on top of your credit card usage and loans. Almost all of your loan applications will be accepted by lenders. You can enjoy increased limits on personal loans and premium cards at an unsecured advantage.

- 650-749: This range showcases that the individuals here have regular payments and manage credit properly. They can get loans approved relatively quickly but with higher interest rates. Getting better terms in the applications may be difficult as the credit score has been affected by one or two missed payments. But nothing too scary.

- 550-649: This range is fair, as individuals under this range might have negative marks on their credit reports. Late and missed payments in the past carry a moderate risk for the lenders when providing the money. People in this category can expect high-interest rates as well.

- 300-549: This poor range indicates a high likelihood of defaulting (not repaying the amount). The factors mentioned above will be harmful to these individuals. Missed payments, defaulting on payments, or very high credit utilisation have significantly reduced the chances of loan approvals.

What if there is no credit history?

If you haven't taken any credit till now, your score will be “No Hit” meaning there isn't enough data to provide a score. It will cause an issue when applying for loans and credit since you cannot be evaluated on your credit behaviour. Building a credit history with responsible credit card use or co-applicant loans is crucial for future financial needs.

So it's essential to have your credit history proper and in a good-excellent range for future financial needs. You can monitor your credit history occasionally, see where you are taking a hit, and take required corrective actions. You can also dispute if you see any issues or wrong data.

In a short sense, there are mainly 4 factors decide your securing a loan: your repayment history, credit utilisation, credit mix (credit types) and your recently sanctioned loans. By managing these so that the scores are always between the range of 650-900 you can enjoy almost all of your loans being approved. The optimal range for your score is between 750-900 where you can not only get your loans approved but also enjoy better interest rates and deals. A score below 550 means you are not trustworthy to provide loans. So you should never let your score drop to this range. There can also be a “No Hit” range where there isn’t enough data to provide you with a score. It is important to manage your credits so that your present and future are secure and prosperous. Check your credit score regularly and manage your credit wisely to secure your financial future.